SMM March 19 News:

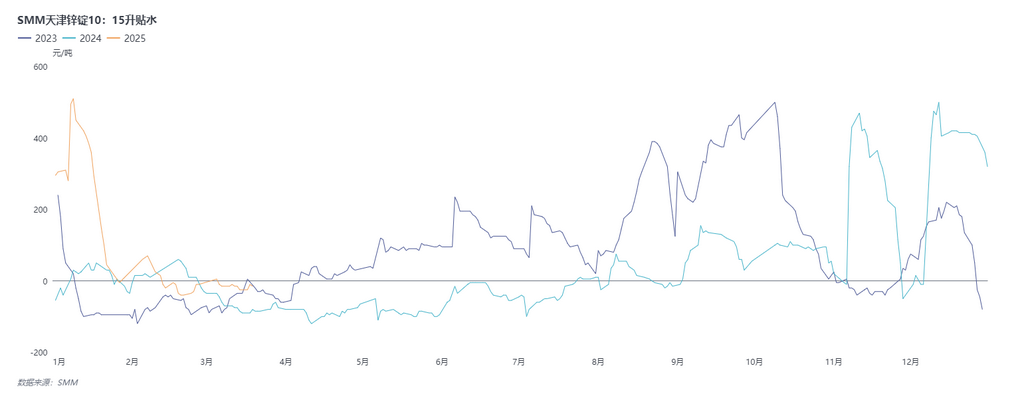

According to SMM communication, the Tianjin region has been operating at small discounts throughout March. What are the reasons behind this? How will premiums and discounts evolve in the future?

SMM provides the following analysis:

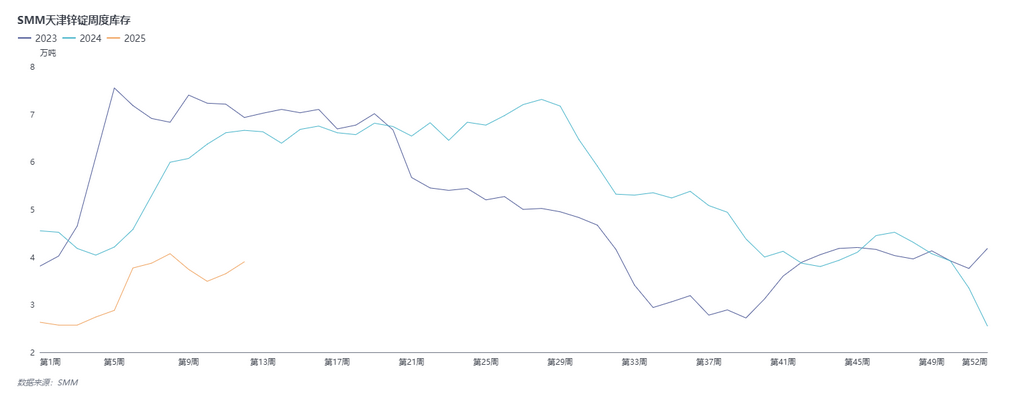

Supply side, the production of mainstream smelters in the Tianjin region was relatively normal in February, with production at approximately 90,000 mt. Some smelters also have plans to increase production, with March production expected to reach around 95,000 mt, indicating an increase in zinc ingot production. The overall spot supply in Tianjin has somewhat eased in March. However, Tianjin zinc ingot inventory remains significantly lower than in previous years, primarily because the long-term contract volume of smelters in 2025 decreased compared to 2024, leading to reduced warehouse storage. Additionally, many zinc ingots were directly shipped to downstream users, resulting in fewer arrivals at Tianjin warehouses. The price gap between self pick-up from warehouses and delivery-to-factory prices widened, reducing downstream procurement of warehouse zinc ingots and making it difficult for premiums to rise.

Demand side, northern consumption slightly improved in March but remained weaker YoY. The "Golden March" effect was not evident. Coupled with environmental protection-driven production restrictions during the Two Sessions in Tianjin and Hebei, enterprise operations were affected. Transportation was also impacted due to requirements for National VI or new energy vehicles. March consumption recovery fell short of expectations, and galvanising enterprises mainly made just-in-time procurement without significant stockpiling, suppressing the trend of premiums and discounts. Overall, premiums and discounts in the Tianjin region struggled to rise.

Looking ahead, sulphuric acid prices are continuously rising, combined with the ongoing increase in zinc concentrate TCs. Smelters have generally turned from losses to profits, boosting production enthusiasm. Zinc ingot production in the Tianjin region is expected to remain strong, with overall spot supply relatively ample. As the Two Sessions conclude, consumption is expected to gradually improve, and downstream purchases of zinc ingots may increase, leading to stable or slightly rising premiums and discounts.

(The above information is based on market data collection and comprehensive evaluation by the SMM research team. The information provided herein is for reference only and does not constitute direct investment research advice. Clients should make cautious decisions and not replace independent judgment with this information. Any decisions made by clients are unrelated to SMM.)